Understanding Prepaid Expenses: Examples & Journal Entry

Content

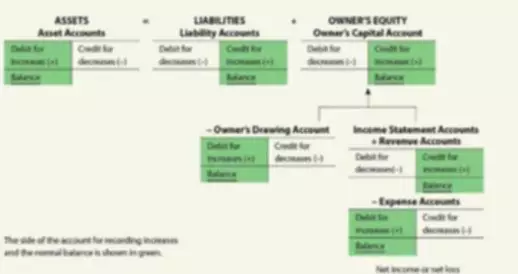

Finally, In the 12th month, the final $15,000 will be fully expensed and the prepaid account will be zero. “Deferred” means “postponed into the future.” In this case you have purchased something in “bulk” that will last you longer than one month, such as supplies, insurance, rent, or equipment. Rather than recording the item as an expense when you purchase it, you record it as an asset (something of value to the business) since you will not use it all up within a month. At the end of the month, you make an adjusting entry for the part that you did use up—this is an expense, and you debit the appropriate expense account. The credit part of the adjusting entry is the asset account, whose value is reduced by the amount used up. Any remaining balance in the asset account is what you still have left to use up into the future.

Here are the Prepaid Rent and Rent Expense ledgers AFTER the adjusting entry has been posted. Here are the Prepaid Insurance and Insurance Expense ledgers AFTER the adjusting entry has been posted. Here is the Insurance Expense ledger where transaction above is posted. Here is the Supplies Expense ledger where transaction above is posted.

Illustration of Prepaid Rent

Initially, she records the transaction by increasing one asset account (prepaid insurance) with a debit and by decreasing another asset account (cash) with a credit. After one month, she makes an adjusting entry to increase (debit) insurance expense for $300 and to decrease (credit) prepaid insurance for $300. The initial journal entry for a prepaid expense does not affect a company’s financial statements. The initial journal entry for prepaid rent is a debit to prepaid rent and a credit to cash. With that, do not allow the term “expenses” in “prepaid expenses” to deceive you. Despite its name, prepaid expenses are not recorded as expenses upon their initial payment.

Is prepaid insurance adjusting entry debit or credit?

Prepaid insurance is usually charged to expense on a straight-line basis over the term of the related insurance contract. When the asset is charged to expense, the journal entry is to debit the insurance expense account and credit the prepaid insurance account.

Prepaid expenses are recognised as a type of asset because they represent products and services whose benefits will only be incurred at a later date. Thankfully though, companies may still drastically lower their risk of encountering minor errors by automating their entire accounting procedure using smart credit control platforms like Kolleno. In summary, Kolleno is an all-in-one software that can be integrated into a business’s existing workflow, with the accounting team being seamlessly onboarded in no time.

Question: What is the 12-month rule for prepaid expenses?

An expense is a cost of doing business, and it cost $100 in supplies this month to run the business. The premium covers twelve months from 1 September 2019 prepaid insurance journal entry adjustments to 31 August 2020, i.e., four months of 2019 and eight months of 2020. It would be incorrect to charge the whole $4,800 to 2019’s profit and loss account.

TIM S A : Independent auditor’s report on the quarterly information – Form 6-K – Marketscreener.com

TIM S A : Independent auditor’s report on the quarterly information – Form 6-K.

Posted: Tue, 09 May 2023 07:00:00 GMT [source]

You accrue a prepaid expense when you pay for something that you will receive in the near future. Any time you pay for something before using it, you must recognize it through prepaid expenses accounting. BlackLine and our ecosystem of software and cloud partners work together to transform our joint customers’ finance and accounting processes. Together, we provide innovative solutions that help F&A teams achieve shorter close cycles and better controls, enabling them to drive better decision-making across the company. Adjusting entries are the journal entries that are posted at the end of each accounting period to adjust the ledger balances for accruals and deferrals required as per the accrual basis of accounting.

Not tracking the expiration date of prepaid expenses

Deferred expenses are payments made for goods or services that will be received in the future. Prepaid income is when a company receives payment in advance for goods or services that they will provide in the future. Prepaid expenses refer to expenses that a business pays in advance before they are actually incurred.

The remaining $6,000 amount would be transferred to expense over the next two years by preparing similar adjusting entries at the end of 20X2 and 20X3. As the amount of prepaid insurance expires, the expired portion is moved from the current asset account Prepaid Insurance to the income statement account Insurance https://www.bookstime.com/articles/prepaid-insurance-journal-entry Expense. This is usually done at the end of each accounting period through an adjusting entry. In order to adjust the entry for prepaid insurance, the amount of expired insurance has to be determined. Once this is done, the amount is recorded as a debit to insurance expense and a credit to prepaid insurance.

Expense Method

BlackLine is a high-growth, SaaS business that is transforming and modernizing the way finance and accounting departments operate. Our cloud software automates critical finance and accounting processes. We empower companies of all sizes across all industries to improve the integrity of their financial reporting, achieve efficiencies and enhance real-time visibility into their operations. Working capital, cash flows, collections opportunities, and other critical metrics depend on timely and accurate processes. Ensure services revenue has been accurately recorded and related payments are reflected properly on the balance sheet. The adjusting journal entry should be passed at the end of every period in order to prepare and present the correct monthly financial statement of the company to the stakeholders.

What is the adjustment entry for insurance?

The adjusting entry ensures that the amount of insurance expired appears as a business expense on the income statement, not as an asset on the balance sheet. IMPORTANT: If this journal entry had been omitted, many errors on the financial statements would result.